In financial services, many firms are focused on providing bottom-line value to their clients. What most of them forget is how to properly communicate that value.

A good PR strategy has a greater impact on the bottom line than most firms realise. This book shows how to put in place an effective PR program in the financial services industry, and how great communications can add significant value to a firm.

Between them, Claudia Pritchitt and Leeanne Bland have over 50 years’ experience in public relations, communications, and marketing. Here, they explain the key tools needed in an effective communications strategy as well as why plain English is imperative in the jargon-heavy world of financial services.

The net reduction of advisers, down by (-32), was the biggest loss since June this year and may be signal what’s in store over the coming weeks. Two new licensees commenced with a total of eight advisers between them. Three licensees ceased.

There were only three new entrants, but we expect the number of new entrants to ramp up once the financial adviser exam results are released later in the month. There were 95 advisers affected this week, a significant jump on recent weeks.

Centrepoint Group moved ahead of Count Limited to become the second-largest advice firm. This week, Centrepoint added two advisers, reaching 589, while Count lost six, dropping to 583. Five of Count’s losses were at Merit Wealth, where most advisers focus only on ‘restricted’ SMSF advice. We expect most restricted SMSF only advisers to cease by 2026.

Key adviser movements for this period

Net change of advisers (-32)

Current number of advisers 15,427

Net change calendar 2025 YTD (-44)

Net change 2025 YTD of +117 when excluding licensees that provide mostly limited SMSF advice

Net change financial YTD (2025/26) +257

Net change financial YTD +280 when excluding licensees that provide mostly limited SMSF advice

16 licensee owners had net gains of 23 advisers

30 licensee owners had net losses for (-55) advisers

2 new licensees, and 3 ceased

3 new entrants

95 advisers affected by appointments / resignations

Growth - licensee owners

One new licensee commenced with five advisers. The advisers switched from Charter, owned by Entireti & Akumin Group

Another new licensee commenced with three advisers, with two advisers switching from Artemis Investments and one from Financial Force

Centrepoint Group is up by net two advisers, appointing five advisers at Alliance Wealth, with three switching from Interprac owned by Sequoia and two coming back into advice after a break of several months. Lost three advisers, two are yet to be appointed elsewhere and one switched to TFG Australia.

A tail of just 13 licensee owners up by net one each including WT Financial Group, Picture Wealth Group and Canaccord

Losses - licensee owners

Entireti & Akumin Group down by eight, six leaving Charter as mentioned above five commencing a new licensee. Fortnum Private and Personal Financial Services losing one each, both not showing as appointed elsewhere and adding one adviser at Fortnum Advice who is coming back into advice after a break of several months.

Count Limited down by six, as mentioned earlier, five of the losses at Merit Wealth, one each at Count Financial and GPS Wealth, none appointed elsewhere and Paragem picking up one adviser who is still showing as being authorised at Perks Private Wealth

Sequoia also down by six, with seven advisers leaving Interprac, three joining Alliance Wealth and the remainder yet to be appointed. One adviser appointed at Interprac, returning after a break of several years from advice.

Koda Capital down by five. However, all five remain at Koda as advisers to wholesale / sophisticated clients only.

Four licensee owners down by two:

Artemis Investments (NSW) joining a new licensee

Finwest Pty Ltd, however, both advisers appear to remain linked to the Finwest group

Mercer and both advisers yet to be appointed elsewhere

Unisuper and both advisers yet to be appointed elsewhere

A tail of 22 licensee owners down by net one each including Bombora Advice, Infocus and Insignia.

Superannuation analysis by fund type to September 2025 APRA recently published its latest superannuation data by fund type, covering the period up to September 2025. We combined this with financial adviser information, population stats from ABS, and SMSF data from ATO.

The data highlights that industry funds continue to dominate. However, retail funds have stabilised while SMSFs continue to be the major beneficiaries of transfers, now mostly out of industry funds.

Net contributions dipped for all fund types this quarter, which is typical due to the previous quarter being June. However, over a rolling 12 months and when compared to 12 months to September 2024, retail funds have increased their net contributions while industry funds have dropped.

Investment returns remain strong across all fund types and retail funds have closed the gap over recent times.

Administration and operating costs remain lower at industry funds as a percentage of assets. However, retail funds have stabilised and generally more competitive that what they were several years ago.

Notes: Re asset allocations - APRA is yet to release asset allocations for this data. ATO detailed SMSF is data yet to be released for this quarter, and we have used an estimate for this quarter.

Key highlights

Growth this quarter and last 12 months - Net assets (for APRA Funds with $50 million or more in assets) increased by $113 billion, from $3,129 billion to $3,242 billion. Over 12 months, net APRA assets are up by $323 billion, moving from $2,919 billion to $3,242 billion.

Investment returns - over the last quarter, retail and industry funds both generated returns of 3.7 per cent each. Over a rolling 12 month period (adding the 4 quarterly returns), industry funds are at 10 per cent and retail funds at 9.4 per cent.

Over five years, industry funds top the returns at 8.5 per cent a year, followed by public funds at 8.1 per cent and retail at 8.0 per cent. For context, in September 2021, industry funds were at 8.6 per cent, public funds at 7.9 per cent and retail funds at 7.0 per cent.

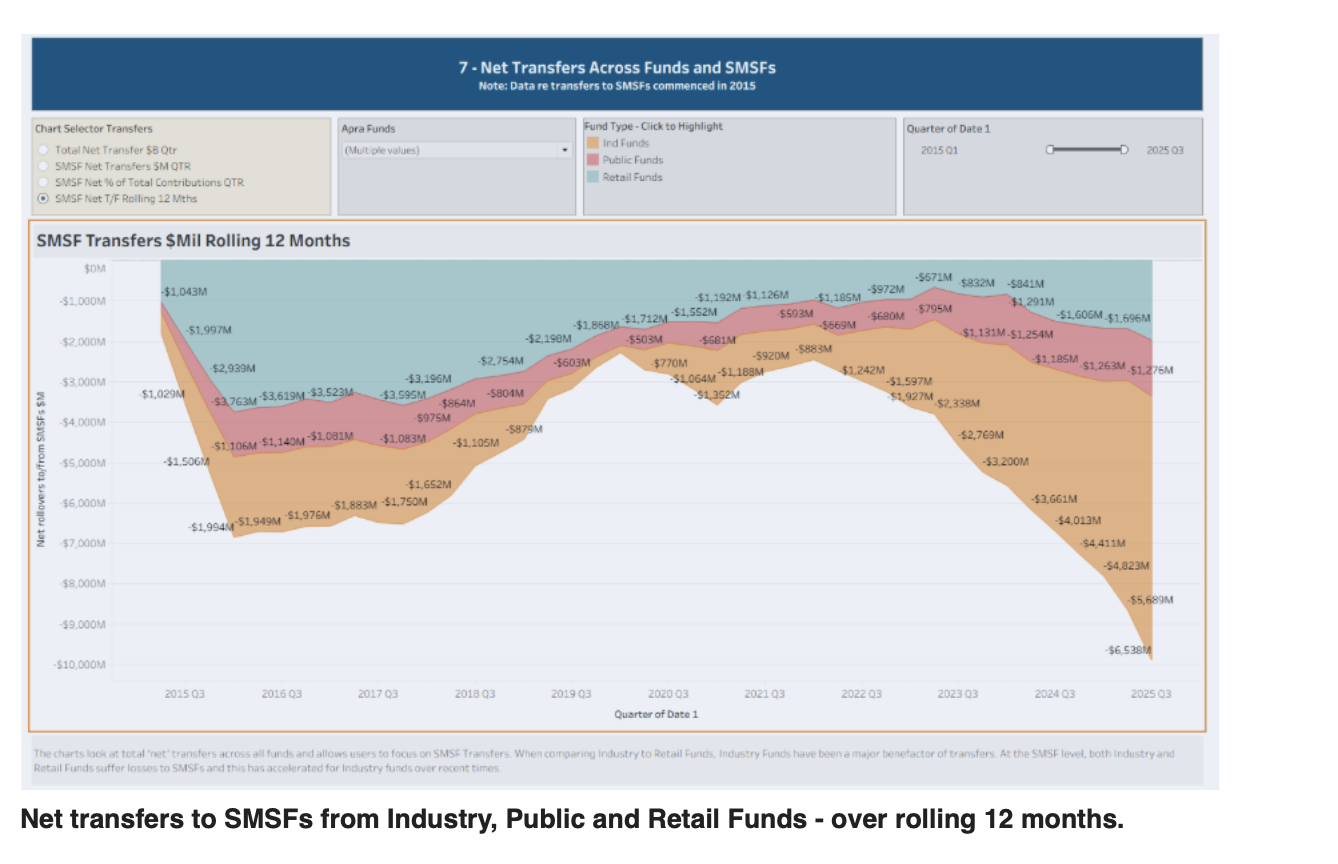

Net transfers to SMSFs (D7) - Net transfers to SMSFs from industry funds continue to grow. For the quarter the net transfers to SMSFs for industry funds is at ( -$2.2 billion), easily the biggest quarter loss to SMSF funds. For the year it is (- $6.54 billion). For context, back in Sept 2023, the yearly amount was (-$1.24 billion)

Retail funds are not immune to losing out to SMSF funds. However, prior to 2021, retail funds made up the largest share of losses and now, over the past 12 months the net loss is (-$1.98 billion) or less than a third of what industry funds lost.

Net contributions - chart shown below - Over the quarter, all fund types had a reduced net flow compared to June which is normal. Over a rolling 12 months, industry funds still dominate at $62.06 billion which below $72.51 billion for the year to September 2024. Retail funds are net at $22.10 billion, almost double what they recorded for 12 months to September 2024 which was at $10.03 billion.

Adviser opportunity - As the number of advisers has steadied, the opportunity in terms of super fund assets per adviser has also steadied. Total assets for APRA and SMSF funds, when divided by the number of advisers as of September 2025, is $270 million per adviser, down slightly from $273 million for June 2025. The main reason for the drop being a strong improvement in the number of advisers since July 1. However, this will probably be short lived due an expected drop in adviser numbers as we enter 2026.

Investment allocation - (updated to June 2025) - industry funds have progressively allocated more to equities. For example, in 2023 Q2 they had 51.9 per cent in equities and now at 57.7 per cent for Q2 2025.